California's Millionaire Tax: What the Surcharge Means for High Earners Now

California’s millionaire tax is easy to overlook until a high-income year brings it directly into view. For California taxpayers with taxable income above $1 million, the state imposes an additional 1% surcharge on income above that threshold. Combined with California’s top marginal rate, federal income tax, and, in some cases, the 3.8% Net Investment Income Tax, the marginal rate on certain income can be materially higher than many taxpayers expect.

Recent legislative proposals in Sacramento have also renewed attention on exit planning, investment structure, income timing, and domicile decisions. Understanding what the surcharge does, and what it does not do, is the starting point for planning.

Cooke Wealth Management works with clients navigating this complexity by connecting financial planning, investment management, retirement planning, and wealth transfer guidance into a coordinated strategy. For high earners evaluating California tax exposure, Cooke Wealth Management's financial planning process can help clarify the real numbers and tradeoffs.

The 1% Surcharge Above $1 Million

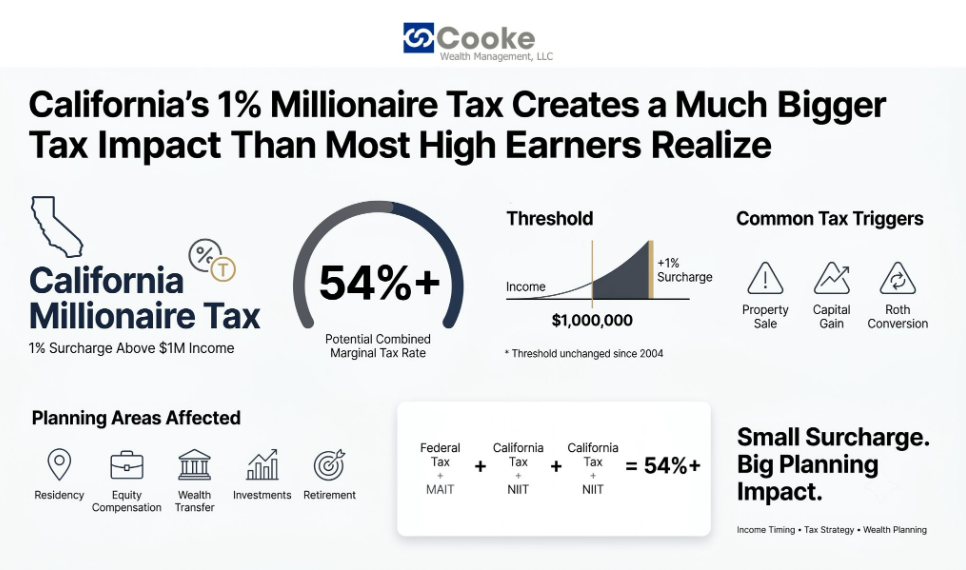

The Mental Health Services Tax, established by Proposition 63 in 2004 and codified in Cal. Rev. & Tax. Code Section 17043, imposes a 1% surcharge on taxable income above $1 million. Stacked on top of California’s 12.3% top marginal rate, the surcharge produces a 13.3% top state marginal rate, identified by the California Franchise Tax Board as California’s highest individual income tax rate.

For some taxpayers, the effect can be significant. A high-income California taxpayer facing the 37% federal bracket, the 13.3% California rate, and the 3.8% Net Investment Income Tax may see an all-in marginal rate above 54% on income subject to all three layers.

The threshold has not moved since 2004. It is not indexed for inflation, unlike California’s regular income tax brackets, which adjust annually under FTB Publication 1031. More taxpayers can become exposed over time without any change to the law.

Sacramento’s Wealth Tax Proposals

The existing surcharge applies to realized income. It does not tax net worth or unrealized gains.

AB 259, introduced in January 2023 by Assembly Member Alex Lee and outlined in his press release, proposed a 1% annual tax on net worth above $50 million and 1.5% on net worth above $1 billion.It died in committee in January 2024. Governor Gavin Newsom also publicly stated that “wealth tax proposals are going nowhere in California.” The proposal would have required a companion constitutional amendment, ACA 3, because California’s constitution places limits on property taxation.

The planning takeaway is not to assume every proposal will pass, but to recognize California’s high-income tax policy remains active.

How the Surcharge WorksThe surcharge applies to California residents with taxable income above $1 million. It can also affect part-year residents and nonresidents with California-source income above the applicable threshold.

California’s capital gains treatment is often the surprise. Per the California Franchise Tax Board, California does not provide a lower rate for long-term capital gains. Capital gains are taxed as ordinary income for California purposes, unlike federal law, where long-term gains may qualify for preferential rates.

For taxpayers near the $1 million threshold, one liquidity event can change the full-year tax picture. A business sale, real estate sale, concentrated stock sale, large K-1 distribution, or substantial Roth conversion may push income above the threshold and trigger the additional 1% surcharge.

Three Planning Mistakes That Quietly Cost Money

First, some taxpayers assume federal capital gains treatment applies at the state level. It does not. A gain that qualifies for a preferential federal rate can still be taxed as ordinary income in California, potentially at the 13.3% top state rate.

Second, Roth conversions should be modeled against California’s surcharge threshold. A conversion that pushes taxable income above $1 million can trigger the extra 1% on the amount above the threshold.

Third, moving out of California does not always end California tax exposure. Deferred compensation, equity compensation, business income, and deferred real estate gains may continue to have California-source consequences after a domicile change.

Before You Move, Convert, or Sell

Residency and Domicile

Per FTB Publication 1031, the 546-day safe harbor applies only to taxpayers absent under a specific employment-related contract, not to general relocation decisions.

The FTB uses a "closest connections" test that examines credit card records, school enrollment, property ownership, medical providers, and social media location data.

A taxpayer who moves to Nevada or Texas may still owe state tax on deferred compensation, vested equity, and business income from California sources. The FTB has four years from the filing date to audit a residency claim, and no statute of limitations applies if no return was filed for a year the FTB believes the taxpayer was a resident.

Equity Compensation Sourcing

California uses a grant-to-vest allocation method for RSUs and a grant-to-exercise method for stock options, as detailed in FTB Publication 1004.

A portion of the income is attributed to California based on the share of days worked in the state during the relevant period, even if the income is recognized years after departure.

This was affirmed in Appeal of Prince (Office of Tax Appeals), in which the FTB applied grant-to-vest sourcing to RSUs that vested two years after the taxpayer became a nonresident. Writers can reference IRS Topic 427 for federal stock option rules as a contrast point.

Roth Conversion Sizing

A conversion counts as ordinary income in California, per the IRS retirement plans FAQs regarding IRAs. A taxpayer with $950,000 in taxable income who converts $100,000 pushes $50,000 over the $1 million mark, incurring the 1% surcharge on that slice on top of the standard rate.

For example: a taxpayer with $950,000 in California taxable income converts $100,000 to a Roth IRA. Only $50,000 of that conversion crosses the $1 million threshold, but that amount now carries both the standard 12.3% rate and the 1% surcharge. Getting the conversion amount right in California requires more precision than in most other states.

QSBS Non-Conformity

Under Section 1202 of the Internal Revenue Code, federal law allows eligible investors to exclude up to 100% of capital gains on qualified small business stock held for five or more years. California explicitly does not recognize this exclusion, as confirmed in the FTB Schedule D (540) Instructions.

A resident who qualifies for the full federal benefit still owes state tax on the entire gain, including the surcharge if total income crosses $1 million. This matters most for startup founders, early employees, and angel investors.

Why Coordinated Planning Matters

Each of these issues becomes more expensive when handled in isolation. A Roth conversion sized without regard to the surcharge, an equity grant exercised without modeling California-source income, or a 1031 exchange completed without considering California’s clawback rules can all create tax consequences that may have been reduced with earlier planning.

Cooke Wealth Management takes a fiduciary approach that connects investment management, retirement planning, wealth transfer guidance, and financial coaching into a single process. For clients navigating California’s tax environment, that can include reviewing income timing, asset location, retirement strategy, charitable giving, and liquidity needs together.

Five Questions California High Earners Should Ask

The following questions are not a self-service checklist. They are a starting point for a planning conversation, a way to identify where exposure exists before a high-income event creates a tax outcome that is harder to address after the fact.

1. What is my projected California taxable income this year, and am I likely to cross the $1 million threshold?

Map every income source: W-2 wages, business income, capital gains, deferred compensation distributions, and any planned Roth conversions.

2. Do I have California-sourced income that would follow me if I changed my domicile?

Equity grants with vesting periods that overlap with California residency, deferred compensation tied to California work, and business interests with California nexus can all remain taxable after a physical move.

3, How does my investment portfolio interact with California's treatment of capital gains as ordinary income?

There is no preferential rate for long-term holdings in California. A portfolio strategy built around federal capital gains planning may need to be reviewed through a California lens.

4. Is there an opportunity to time income recognition, charitable contributions, or Roth conversions to smooth surcharge exposure across multiple years?

California has no income-averaging provision, so this planning must happen before the tax year ends.

5. Have my estate planning documents and beneficiary designations been reviewed in light of California's evolving approach to high-income taxation?

Wealth transfer structures that worked well under prior assumptions may interact differently with ongoing legislative proposals.

The Surcharge Is Not Going Away, But Its Impact Is Manageable

The California millionaire tax has been part of the state's revenue structure for more than two decades, and the defeat of AB 259 did not resolve the fiscal and political pressures that produced it. For high-income households in California, the question is not whether the surcharge applies but how decisions around income timing, investment structure, residency, and retirement accounts interact with it.

That is not a question any one of those decisions answers on its own. It is a planning question, and it benefits from an advisor who can hold the full picture at once.

If you are evaluating how California's tax structure intersects with your retirement strategy, investment portfolio, or wealth transfer plans, Cooke Wealth Management can help you work through the moving parts with a plan built around your priorities.

Frequently Asked Questions

Does the $1 million threshold apply separately to each spouse if a married couple files separately?

Under California Revenue and Taxation Code Section 17043, married taxpayers filing separately each face a $500,000 threshold, not $1 million, before the surcharge applies. The combined exemption for the couple remains $1 million either way, so filing separately does not reduce total surcharge exposure.

California's community property rules add another layer: if income is community property, each spouse must report 50% of it regardless of filing status, which limits the practical flexibility of the separate-filing approach.

There is also an estimated tax consequence: taxpayers whose California AGI exceeds $1 million, or $500,000 filing separately, lose access to the prior-year safe harbor and must instead pay 90% of their current-year tax liability to avoid an underpayment penalty, per California Revenue and Taxation Code Section 19136.3.

Does California tax long-term capital gains differently from ordinary income?

Per the FrCalifornia anchise Tax Board, California does not offer a lower rate for long-term capital gains; all gains are taxed as ordinary income, regardless of how long the asset was held. This contrasts with federal law, which applies preferential rates of 0%, 15%, or 20% based on income.

California voters passed Proposition 1 in March 2024, which renamed the Mental Health Services Act, the 2004 law funding the 1% surcharge, the Behavioral Health Services Act (BHSA) and expanded its scope to include substance use disorder treatment. The surcharge rate and threshold were not changed by Proposition 1.

If I do a 1031 exchange out of California into another state, does California's tax follow me?

Yes. Under California Revenue and Taxation Code Sections 18032 and 24953, taxpayers who sell California property in a 1031 exchange and acquire out-of-state replacement property must file Form FTB 3840 annually until the deferred gain is recognized.

When the replacement property is eventually sold in a taxable transaction, California taxes the original deferred gain, even if the taxpayer no longer lives in California. This clawback provision can result in owing state tax to both California and the state where the replacement property is located.

Can income timing strategies help avoid the surcharge altogether?

In some cases, yes. Strategies such as installment sales (see IRS Publication 537), deferred compensation arrangements, and carefully timed stock option exercises can spread income recognition across multiple tax years to keep any single year's taxable income below $1 million.

There is no income-averaging provision in California that allows retroactive spreading of gains after the tax year ends, so this planning must happen in advance. One frequently overlooked complication: California's estimated tax schedule is front-loaded differently from the federal schedule, per the FTB's estimated tax guidance.

California requires 30% of the annual estimated payment by April 15, 40% by June 15, nothing in September, and 30% by January 15, compared to the federal 25% per quarter. Taxpayers who assume the two schedules match may underpay early and face a penalty even if they pay the correct total by year-end.

Does California recognize the federal QSBS tax exclusion?

California does not conform to Section 1202 of the Internal Revenue Code, so residents who qualify for a full federal QSBS exclusion still owe state tax on the entire gain.

Stock in qualifying C-corporations held for at least five years may be fully sheltered at the federal level while remaining fully taxable in California.

Where does the surcharge revenue go?

Revenue from the 1% surcharge funds the Behavioral Health Services Fund, previously called the Mental Health Services Fund before California voters renamed it under Proposition 1 in March 2024, which supports county-level mental health and substance use disorder programs.

The Legislative Analyst's Office reported $3.3 billion collected for fiscal year 2022-2023, though annual totals swing sharply based on capital gains activity and stock market performance. The surcharge accounts for roughly one-third of county behavioral health services funding in California