California Capital Gains Tax: Why There's No Preferential Rate and What to Do About It

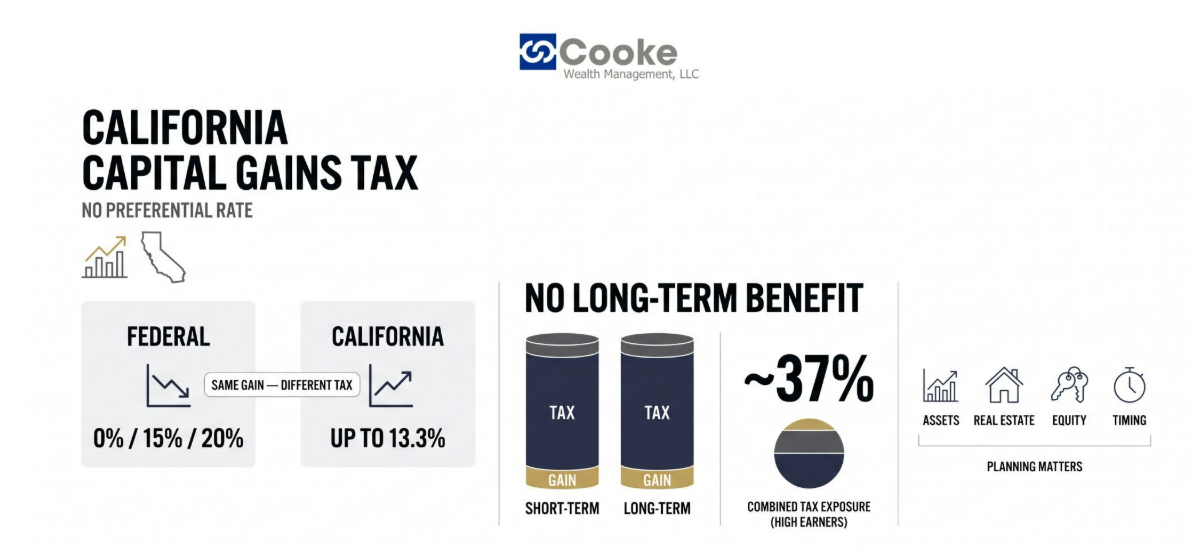

California capital gains tax works differently from the federal system, and for many investors, that gap carries real financial weight. While federal law generally gives long-term capital gains preferential rates, California does not. The state generally treats capital gains as ordinary income, taxed at the same marginal rates that apply to wages and other income.

For higher-income California residents, that difference can carry real financial weight. A major sale may involve federal long-term capital gains tax, California income tax, and, in some cases, the 3.8% Net Investment Income Tax. The result can be a meaningfully higher combined tax cost than many investors expect.

According to the Tax Foundation, that places California among the highest combined capital gains tax jurisdictions in the developed world, above most OECD countries that apply preferential rates to long-term investment gains.

For California investors navigating a major sale, a portfolio transition, or a liquidity event, understanding how the state taxes investment gains is a necessary starting point. Cooke Wealth Management's financial planning and investment management services are designed to help clients think through the timing, structure, and coordination of these decisions before they become taxable surprises.

The Rule California Investors Often Learn Too Late

California capital gains tax is the state income tax applied to profits from the sale of capital assets: stocks, bonds, real estate, business interests, and other investments. Unlike federal tax law, which distinguishes between short-term gains (held less than one year) and long-term gains (held more than one year, taxed at lower preferential rates), California makes no such distinction.

Under California Revenue and Taxation Code Section 18151, all capital gains are included in a taxpayer's ordinary income and taxed at the state's standard marginal rate. That top rate of 13.3%, per the California Franchise Tax Board, is composed of two parts: a 12.3% base rate and a 1% Mental Health Services Tax (established by Proposition 63) that applies to taxable income above $1 million.

Taxpayers approaching that threshold should note that the surcharge applies to all income above $1 million, gains included.

This means a California resident who holds a stock for 20 years and sells it at a $500,000 gain receives no state-level tax benefit for the holding period. The gain is taxed as if it were a paycheck.

Most U.S. states either exempt capital gains from income tax, apply a lower rate, or conform to the federal preferential structure. California is one of only a handful that apply full ordinary income tax rates to investment gains, which is precisely why state-level planning matters more here than almost anywhere else in the country.

The Real Cost of Selling in California

The absence of a preferential state rate does not change what investors owe at the federal level, but it does change the total picture. A California resident selling stock faces federal long-term capital gains tax, the state's ordinary income rate, and potentially the 3.8% NIIT simultaneously.

For higher earners, the combined rate can approach 37%. That math has direct implications for how investors structure decisions:

Charitable Giving Strategies Donating appreciated stock directly to a qualified charity avoids recognition of the gain entirely, bypassing both federal and state tax on the appreciation. This approach often produces a better combined outcome than selling and donating the proceeds.

Opportunity Zone Investments Opportunity Zone investments can defer or reduce federal gain recognition. California does not conform to this provision, however, so state tax on the deferred gain remains due in the year of the original sale.

Tax-Loss Harvesting Tax-loss harvesting can carry amplified value in California because harvested losses offset gains taxed at combined federal and state rates — a larger benefit than in lower-tax states.

Installment Sales Installment sales under IRC Section 453 spread recognition across multiple years, which may reduce the portion taxed at peak marginal rates. This approach also introduces exposure to future rate changes, a relevant consideration given California's legislative history on the subject.

According to the IRS, taxpayers must report capital gains on Schedule D of Form 1040, and California requires a parallel reporting structure on Schedule D (California).

Short-Term vs. Long-Term: A Distinction That Matters Federally, Not in California

At the federal level, holding an asset for more than 12 months converts a short-term gain into a long-term gain, reducing the applicable rate significantly. California provides no parallel benefit. A gain held for 30 days and a gain held for 30 years are taxed identically at the state level. Investors focused on federal tax efficiency may still face significant state exposure regardless of holding period.

Equity compensation often adds another layer. Restricted stock units are generally taxed as compensation when they vest. A later sale of the shares creates a separate capital gain or loss based on the difference between the sale price and the value used at vesting. Stock options can be even more technical, especially when residency changes or California workdays are involved.

Investors expecting a large gain should also review estimated tax obligations. Waiting until tax filing season can create avoidable cash-flow pressure or underpayment penalties. The California Franchise Tax Board's Publication 1004 provides specific guidance on stock option and RSU taxation for state residents.

The Role of Basis and Its Legislative Uncertainty

Gains are calculated on the difference between the sale price and the cost basis of the asset. Basis includes the original purchase price plus any qualifying improvements, and it can be adjusted by events such as stock splits, reinvested dividends, or inheritance.

Inherited assets receive a step-up in basis to fair market value at the date of the decedent's death under IRC Section 1014, which eliminates the built-in gain for the heir. Federal proposals have periodically sought to limit or eliminate this rule, and its long-term status is not guaranteed.

That uncertainty is worth weighing before assuming the step-up will be available when an estate is eventually settled. Gifts of stock or other assets do not receive a step-up. The recipient takes the donor's original basis, which may affect the tax outcome when the position is eventually sold.

Estimated Tax Payments

California requires taxpayers with significant capital gains to make estimated quarterly tax payments to the Franchise Tax Board. Failure to pay sufficient estimated taxes may result in underpayment penalties.

Investors anticipating a large gain from a scheduled sale should coordinate payment timing with a tax advisor before the transaction closes.

The Details That Determine Whether Your Strategy Works

Several interconnected factors shape the real cost of a gain and the value of any mitigation strategy:

Residency Timing

California taxes gains earned by residents regardless of where the assets are held. Investors who establish residency outside the state before selling may avoid the state tax, but the Franchise Tax Board applies a sourcing analysis to certain asset types, including interests in California businesses and real property.

Residency changes require careful documentation and should not be treated as a guaranteed avoidance strategy.

Federal Conformity Gaps

Beyond the Opportunity Zone rules noted earlier, California does not conform to the Qualified Small Business Stock (QSBS) exclusion under IRC Section 1202. That provision allows investors in qualifying small businesses to exclude up to 100% of federal capital gains on stock held more than five years.

California provides no equivalent, meaning founders and early-stage investors may owe full state income tax on gains that are entirely exempt at the federal level.

Proposition 19 and Inherited Real Estate

Effective February 2021, Proposition 19 significantly narrowed the parent-child property tax transfer exclusion. Prior law allowed children to inherit a parent's assessed value on both a primary residence and other properties.

Under Proposition 19, the exclusion is largely limited to a primary residence, and only if the child uses it as their own primary residence within one year. Families with significant real estate holdings should review how this change affects both property tax and gain planning under the guidance of the California State Board of Equalization.

Home Sale Exclusion

California conforms to the federal home sale exclusion under IRC Section 121: $250,000 for single filers and $500,000 for married filing jointly. This can reduce or eliminate gain on a primary residence sale. Gains on investment real estate do not qualify and are taxed at California's ordinary income rates.

California-Specific Issues That Can Change the Plan

Capital gains tax rarely exists in isolation. It intersects with portfolio structure, retirement income, estate goals, charitable intent, and the timing of major transactions. For California residents, the absence of a preferential state rate makes that coordination more consequential.

Cooke Wealth Management provides financial planning, investment management, retirement planning, and wealth transfer guidance to clients working through these decisions. The firm's fiduciary approach reflects each client's complete situation, not just the mechanics of a single transaction.

For a client approaching a liquidity event, that may mean reviewing how a sale interacts with retirement income, estimated tax obligations, and charitable giving goals before anything closes.

For a client managing equity compensation, it means distinguishing the ordinary income event at vesting from the gain event at sale and preparing for both.

For a client with real estate, it may mean analyzing how Proposition 19 has changed the inherited property equation and whether holding, selling, or transferring serves their goals.

Cooke does not guarantee tax outcomes, and every situation requires coordination with a qualified tax advisor. What the firm offers is a planning process that accounts for California's tax environment from the beginning, not as an afterthought.

Five Questions to Ask Before You Sell

Before making a major investment sale, California residents can work through this sequence to identify where guidance adds the most value:

1. What is the full gain, and over what holding period?

Calculate the difference between anticipated sale price and cost basis. Confirm whether the gain is short-term or long-term for federal purposes, recognizing that the distinction does not affect the state rate.

2. What is the estimated combined rate?

Add the applicable federal long-term rate, the 3.8% NIIT if income thresholds apply, and California's marginal rate, including the 1% Mental Health Services Tax surcharge if total income will exceed $1 million in the year of sale.

3. Is there a charitable giving structure that fits?

Donating stock directly to a qualified charity avoids recognition of the gain. Donor-advised funds allow donors to make a contribution in a high-income year and distribute grants over time, separating the tax event from the philanthropic decision.

4. Does the timing interact with other income?

A large gain recognized in the same year as a Roth conversion, RSU vesting event, or deferred compensation distribution can push total income into higher marginal brackets. An installment sale under IRC Section 453 may reduce the effective rate, though the tradeoff is exposure to future changes in California's rate structure.

4. Have estate planning implications been reviewed?

The step-up in basis under IRC Section 1014 can make holding long-appreciated assets more efficient than selling. Given ongoing federal legislative interest in modifying this rule, the analysis should happen sooner rather than later, in consultation with both a financial planner and an estate attorney.

You Can't Change the Rate. You Can Change the Plan.

California capital gains tax is a fixed feature of investing in this state. It does not respond to willpower or wishful accounting. But it does respond to planning, and the difference between a reactive sale and a coordinated strategy can be significant.

The investors most exposed to California's combined tax burden are often those with the most options: long-held positions, equity compensation, charitable capacity, and the flexibility to time major transactions. The challenge is identifying which options apply and acting on them before the sale closes.

If you are facing a major transaction, managing a concentrated position, or trying to understand how California's tax treatment fits into a broader financial plan, Cooke Wealth Management can help you work through the specifics. Reach out to schedule a discovery conversation.

Frequently Asked Questions

Are capital gains from selling a rental property in California taxed differently than stock gains?

The California rate structure is generally the same, but rental property can add federal depreciation recapture, basis adjustments, and real estate-specific planning issues. Long-held rental property should be modeled before assuming the tax result will resemble a stock sale.

Does California tax capital gains earned by a trust or estate?

Yes. California taxes capital gains earned by a trust or estate at the same ordinary income rates that apply to individuals, with a top rate of 13.3%, per the California Franchise Tax Board's estates and trusts guidance.

The more important planning detail is that trusts reach California's highest bracket far sooner than individuals. The compressed tax bracket structure means the top marginal rate applies at a much lower income threshold than the $1 million threshold for individuals.

Under California Revenue and Taxation Code Section 17742, a trust with a California-resident trustee or non-contingent beneficiary may owe California income tax on capital gains even if the grantor is no longer a California resident, making trustee selection and beneficiary structure meaningful planning variables.

Can a Charitable Remainder Trust help reduce California capital gains tax on a large asset sale?

A Charitable Remainder Trust (CRT) may defer gain recognition and support charitable goals when structured properly. However, distributions to beneficiaries can still carry taxable income, and the benefit depends on the donor’s charitable intent, income needs, tax rates, and trust design.

Can a Charitable Remainder Trust help with a large asset sale?

California's clawback provision, codified under California Revenue and Taxation Code Sections 18032 and 24953, requires investors who exchange California real property for out-of-state replacement property under IRC Section 1031 to continue reporting the deferred gain to California annually until it is recognized.

Even if the investor moves out of California and sells the replacement property in another state, California asserts the right to tax the original California-sourced gain at that time.

The mechanism is Form FTB 3840, which must be filed every year the replacement property is held. Failure to file can result in a Notice of Proposed Assessment from the FTB estimating the full deferred gain as taxable income, plus penalties and interest. This makes annual compliance a material obligation for any investor who has exchanged out of California.

What happens to California capital gains tax if an asset was partially acquired before moving to California?

California uses an apportionment method for certain assets acquired before a taxpayer became a California resident. For stock options and RSUs in particular, California taxes only the portion of the gain corresponding to the time the employee worked in California relative to the total vesting period, per the California Franchise Tax Board's Publication 1004 on equity-based compensation.

Federal tax applies to the full gain regardless of where the work was performed. California's apportionment rules can reduce, though rarely eliminate, state exposure for employees who moved to California partway through a vesting schedule. Accurate documentation of work location during the vesting period is necessary to support the apportionment calculation.

Can prior capital losses offset California gains?

Often, yes. California generally follows capital loss carryover concepts, so unused losses may help offset future gains. Prior-year returns should be reviewed before assuming a new sale starts from a clean tax slate.