Fee-Only Fiduciary Financial Advisor Servicing Inland Empire

If you are searching for a fee-only fiduciary financial advisor, you already know the core issue: you want advice from someone who is paid directly by you, legally obligated to put your interests first, and not compensated by product commissions.

The harder part is verifying that standard before you commit. The Inland Empire has no shortage of financial professionals, but “fiduciary” and “fee-only” are specific legal and compensation distinctions, not interchangeable marketing terms.

Cooke Wealth Management is a fee-only fiduciary firm serving individuals and families across Southern California, including clients in the Inland Empire. The firm provides financial planning, retirement planning, investment management, wealth transfer guidance, and financial coaching for clients working through major financial decisions. If you are ready to start that conversation, you can schedule a discovery session with Cooke Wealth Management.

Two Words That Mean Something Specific (and One That Doesn't)

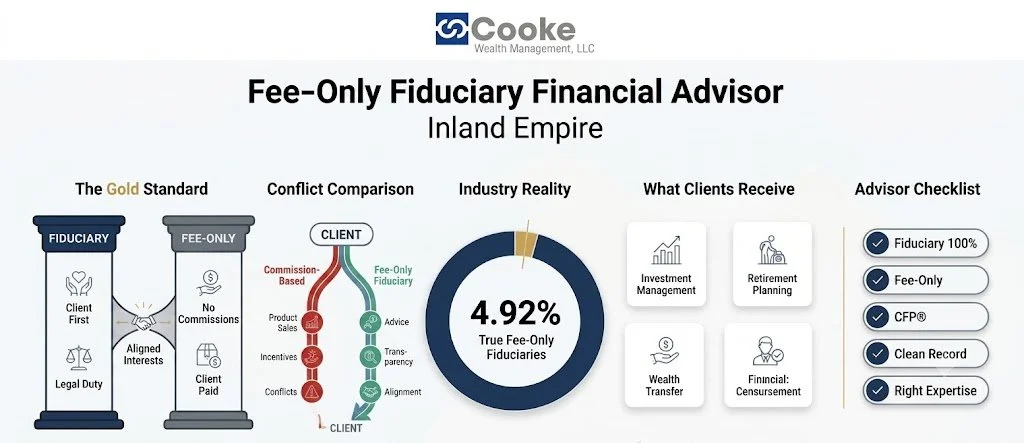

Fiduciary is a legal standard. Under the Investment Advisers Act of 1940, registered investment advisers generally owe clients a fiduciary duty. The SEC has described that duty as including both a duty of care and a duty of loyalty. The Supreme Court’s decision in SEC v. Capital Gains Research Bureau also emphasized the importance of disinterested advice and disclosure of material conflicts.

In practice, fiduciary duty means the advisor must act in the client’s best interest, disclose material conflicts, and avoid placing the advisor’s interests ahead of the client’s.

Fee-only is a compensation structure. According to NAPFA, fee-only advisors are compensated directly by clients and do not accept commissions for their work. Compensation may be structured as a flat fee, retainer, hourly fee, or percentage of assets under management.

Together, these standards describe an advisory relationship designed to reduce product-sales conflicts. The word “advisor,” by contrast, is not enough on its own. Consumers still need to verify how the professional is registered, how they are paid, and what standard applies.

The Conflict You May Not See at the First Meeting

The difference between a fiduciary and a non-fiduciary relationship may not be obvious at the first meeting. It often becomes clearer when recommendations are made.

A commissioned professional may earn more when a client purchases a particular annuity, insurance product, mutual fund share class, or other financial product. That does not mean every commissioned advisor acts in bad faith. It means the compensation structure creates a conflict that should be disclosed and understood.

Dual registration can make this more confusing. Some professionals operate as both investment adviser representatives and broker-dealer representatives. In one capacity, they may provide advisory services under a fiduciary framework. In another, they may recommend products under broker-dealer rules. SEC guidance recognizes that these standards can apply differently depending on the capacity in which the professional is acting.

That is why the better question is not simply, “Are you a fiduciary?” It is, “Are you a fiduciary 100% of the time when working with me?”

Fee-only fiduciaries are also less common than the marketing language suggests. A Human Investing analysis, drawing on Bureau of Labor Statistics and FINRA data, estimated that only 4.92% of financial professionals operate as true fee-only fiduciaries.

What the Relationship Looks Like Day to Day

A fee-only advisory relationship should make compensation clear. According to Kitces research on advisor fees, common models include flat retainers, hourly fees, and assets-under-management fees. The exact structure varies by firm and service level, but the key is that the client can see who is paying the advisor and why.

In a genuine fee-only relationship, you should not see insurance commissions, fund-company trailing payments, product-sales compensation, or referral payments from third parties.

The planning process is also broader than portfolio management. Most engagements begin with a review of income, assets, liabilities, insurance, tax exposure, estate documents, retirement projections, and family priorities. The relationship is ongoing rather than transactional. The goal is better decision-making over time, not a one-time product sale.

Vanguard’s Advisor’s Alpha research has long emphasized that the value of advice often comes from behavior, structure, and discipline rather than stock selection alone. An advisor’s ability to help clients stay aligned with a plan during market stress can be meaningful, especially when that advisor has no product incentive pulling the recommendation in another direction.

What to Ask Before You Commit

Start with direct questions.

Are you a fiduciary 100% of the time when working with me?

Are you fee-only, or do you receive commissions, referral fees, revenue sharing, or other third-party compensation?

Are you registered as an investment adviser, a broker-dealer representative, or both?

Can I review your Form ADV?

The SEC’s Investment Adviser Public Disclosure database allows investors to review registered investment advisers and their Form ADV filings. FINRA BrokerCheck allows investors to review broker-dealer registration and disclosure history. Both tools are worth checking before signing an advisory agreement.

Before You Sign Anything: Five Things Worth Checking

1. Minimum Asset Thresholds

Some firms require significant investable assets to take on a new client. Others work with clients earlier in the accumulation phase. Ask clearly whether you qualify before investing time in the process.

2. Specialty and Scope

A retirement income specialist and a comprehensive financial planner serve different functions at different price points. Confirm the advisor works on the issues you are bringing, whether that is retirement planning, tax coordination, estate transfers, investment management, or financial coaching.

3. The CFP Designation and What it Now Requires

In June 2020, the CFP Board strengthened its Code of Ethics, expanding the fiduciary obligation for Certified Financial Planners from "when providing financial planning" to "at all times when providing any financial advice." That is a broader and more meaningful standard than what applied before 2020.

Verify current certification status through the CFP Board's public verification tool.

4. Regulatory History

Check credentials and complaint history through FINRA BrokerCheck and the SEC's Investment Adviser Public Disclosure database before committing. A clean record is a baseline, not a differentiator, but the absence of one is a clear signal.

5. Values Alignment

Planning involves decisions about priorities, legacy, risk tolerance, and family dynamics that go beyond the numbers. An advisor whose approach fits your values is more likely to give you guidance you will follow through on.

Where Cooke Wealth Management Fits Into This Picture

Cooke Wealth Management is a fee-only fiduciary firm based in Irvine and serving clients across Southern California, including families in the Inland Empire. The firm provides financial planning, investment management, retirement planning, wealth transfer guidance, and financial coaching with a values-aligned planning approach.

Cooke’s financial coaching service may be a fit for clients who are not yet ready for full investment management but want help building better financial habits, understanding options, or preparing for a major financial decision.

For clients near or in retirement, Cooke’s retirement planning services can address income sequencing, Social Security timing, required minimum distributions, and tax-aware withdrawal strategies. The firm’s broader financial planning process can also help coordinate investments, cash flow, estate considerations, and long-term family priorities.

For clients who want financial decisions to reflect faith, stewardship, family goals, or charitable intent, Cooke’s values-driven approach may provide a more personal planning framework than a purely numbers-driven model.

Five Questions That Separate a Real Fiduciary From a Good Pitch

Before committing to any advisory relationship, work through these:

1. Are you a fiduciary 100% of the time?

Ask for written confirmation. If the answer is qualified in any way, ask what it is qualified by and what standard governs those other engagements.

2. Are you truly fee-only?

Ask: "Do you or your firm receive any compensation other than what I pay you directly?" The answer should be an unqualified no. Cross-reference their Form ADV to verify.

4. What credentials do you hold?

The CFP designation now requires adherence to the fiduciary standard at all times when providing financial advice. Verify current standing through the CFP Board's verification tool.

5. Does your scope match my situation?

Confirm the advisor works on your specific issues: retirement income, tax strategy, estate coordination, insurance review, or behavioral coaching, not just investment management.

6. What does your regulatory record show?

Run every advisor through FINRA BrokerCheck and the SEC's IAPD database before signing anything.

You Asked the Right Question: Here's the Right Next Step

Knowing what to look for is the first step. Finding a firm that meets the standard and fits your situation is the next.

If you are working through retirement decisions, investment questions, wealth transfer planning, or simply trying to understand where you stand, Cooke Wealth Management’s services are built around planning first, not product recommendations. A discovery conversation can help clarify whether the relationship is the right fit

Frequently Asked Questions

Are financial advisory fees tax-deductible?

For most individuals, investment advisory fees are generally not deductible as miscellaneous itemized deductions under current federal law. The Tax Cuts and Jobs Act suspended many miscellaneous itemized deductions, including investment expenses and investment management fees. Tax rules can change, and exceptions may apply in limited circumstances, so clients should confirm their specific treatment with a tax professional.

What is the difference between a fee-only and a fee-based advisor?

A fee-only advisor is compensated only by client fees. A fee-based advisor may charge client fees but may also receive commissions or other compensation from financial products. The distinction matters because it affects whether product-related incentives may influence a recommendation.

What life events typically signal it's time to engage a fiduciary planner?

Common triggers include approaching retirement, receiving an inheritance, selling a business, going through divorce, changing jobs, exercising equity compensation, starting a family, or losing a spouse. These events can affect taxes, beneficiary designations, insurance, cash flow, and estate documents. Planning before a major decision is generally more effective than trying to correct an uncoordinated decision later.

Social Security is one example. Workers born in 1960 or later who claim retirement benefits at age 62 generally receive 70% of their full retirement benefit, while delaying to age 70 can increase the benefit to 124%. That decision interacts with retirement income sequencing, tax planning, and spousal benefit strategy.

What happened to the DOL's 2024 Retirement Security Rule, and does it affect me?

In March 2026, the U.S. Department of Labor restored the long-standing five-part test for determining investment-advice fiduciary status after court decisions vacated the 2024 Retirement Security Rule. The practical takeaway is that rollover and retirement-account advice can depend heavily on the advisor’s status, capacity, and applicable rules. Working with a firm that independently operates as a fiduciary can provide a clearer standard than relying only on shifting regulatory requirements.

Can a fee-only fiduciary help with more than investment management?

Yes. Comprehensive fee-only planning can include retirement income sequencing, Social Security claiming strategy, tax-aware withdrawal planning, insurance review, beneficiary and estate coordination, charitable giving, and financial coaching. The broader the decision, the more important it is that advice be coordinated rather than isolated.

What does "values-aligned" financial planning mean?

Values-aligned planning connects financial decisions to a client’s broader priorities, including family goals, charitable intent, legacy, stewardship, and personal principles. For some clients, that may include a faith-based view of responsibility and generosity. The purpose is to build a plan that reflects both the numbers and the life those numbers are meant to support.